✅ Strategically choosing trade shows and showrooms that align with your target audience can significantly boost brand visibility and lead generation.

✅ Setting measurable goals (like specific lead counts or partnership opportunities) and closely monitoring ROI ensures better budgeting and long-term success.

✅ Effective pre-show marketing, well-trained staff, interactive booth designs, and consistent post-event follow-up are crucial factors in converting event attendees into lasting business relationships.

Wholesalers often sell products in bulk to retailers or other distributors, navigating large invoices, extended payment terms, and unpredictable demand swings. Emerging brands, sales leaders, and wholesale managers must develop strong financial foundations to keep operations running and plan for growth. This guide explores the core principles of wholesale finance—from cash flow and pricing strategies to inventory and risk mitigation—so you can maintain daily liquidity and position your business for long-term success.

Introduction

Running a wholesale operation differs significantly from retail. In wholesale, you buy inventory in large quantities and sell it to retailers or other wholesalers at a markup. This bulk model often means:

- Bigger capital requirements upfront

- More complex logistics and inventory management

- Greater vulnerability to delayed customer payments

A solid financial architecture helps you manage common hurdles like invoice delays and seasonal spikes. By prioritizing effective cash flow oversight, strategic pricing, and lean operations, you can keep your wholesale business healthy and resilient, even when market conditions fluctuate.

Understanding Wholesale vs. Retail

Wholesalers focus on moving larger quantities of goods to business clients, whereas retailers sell smaller amounts directly to consumers. Here’s a quick comparison:

| Aspect | Wholesale | Retail |

|---|---|---|

| Customers | Sells to retailers or other wholesalers | Sells directly to end consumers |

| Volume | Larger order sizes, bulk logistics | Smaller, more frequent consumer transactions |

| Payment | Often Net 30 or Net 60 terms | Generally immediate or short-term payments from buyers |

| Key Focus | Pricing, inventory management, ensuring adequate supply | Marketing, merchandising, customer experience |

While profit margins for wholesalers can be slender—averaging about 3.2% of revenue—a well-tuned approach to supply costs, payment terms, and logistics can keep your operation viable.

The Role of Financial Management

Effective financial management underpins every wholesale operation. Large-scale inventory purchasing, combined with the possibility of delayed receivables, requires consistent oversight:

- Cash Flow Tracking: Monitor daily inflows and outflows to detect potential bottlenecks.

- Budgeting & Forecasting: Align seasonal demand patterns with your purchasing schedule to avoid over-stocking or running out of popular items.

- Receivables & Payables: Maintain disciplined accounts receivable policies, and negotiate favorable terms with suppliers.

Wholesalers often measure success by how quickly they convert purchases back into cash. The average wholesale distributor has a cash-to-cash cycle of 56.3 days. Regularly reviewing your cycle time helps you catch slow payments or inventory buildup before they jeopardize liquidity.

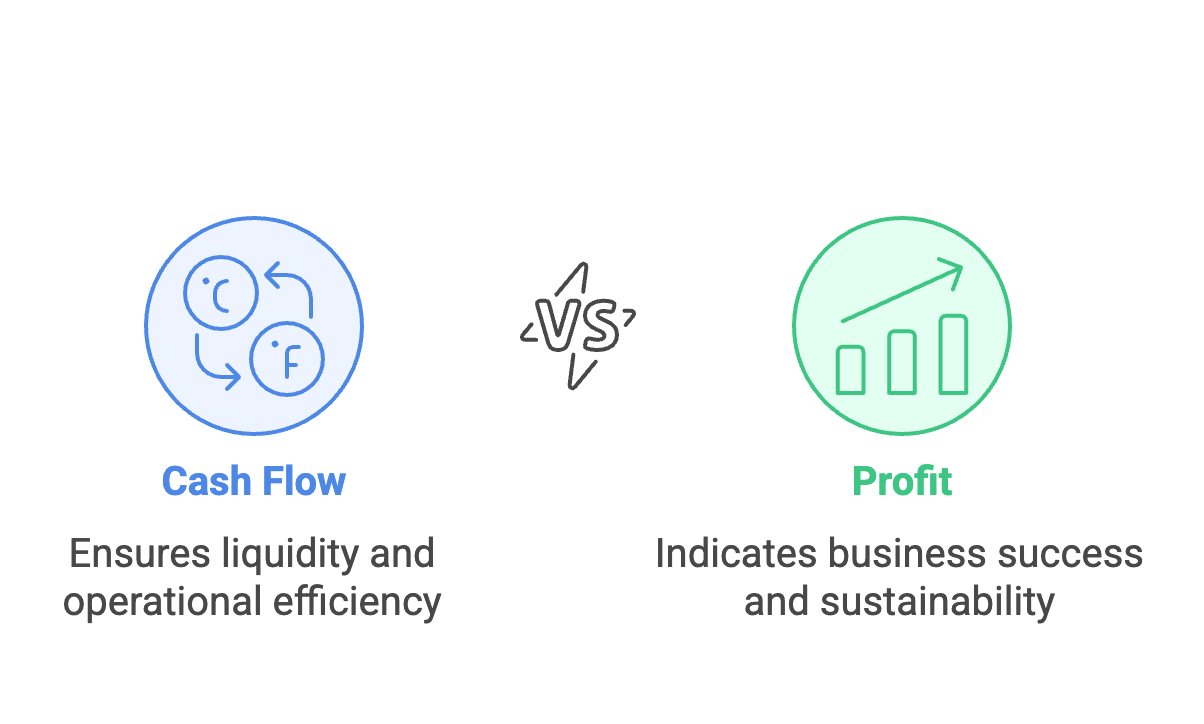

Cash Flow vs. Profit

It’s possible for a wholesale business to appear profitable—yet struggle to pay bills on time. This happens when revenue looks good on paper, but actual cash is tied up in unsold stock or unpaid invoices. Common scenarios that create these gaps include:

- Extended Payment Terms: Offering Net 60 or Net 90 can secure big customers, but delays your own cash inflows.

- Seasonal Demand Fluctuations: Stocking early for peak seasons can divert funds prematurely.

- Large Bulk Orders: Buying inventory in volume may improve unit costs but can lock up capital until those goods are sold.

Approximately 61% of small wholesale businesses experience cash flow challenges linked to late customer payments. Regular cash flow analysis—not just profit-and-loss statements—reveals if you’ll have enough funds to pay suppliers, staff, and operating costs.

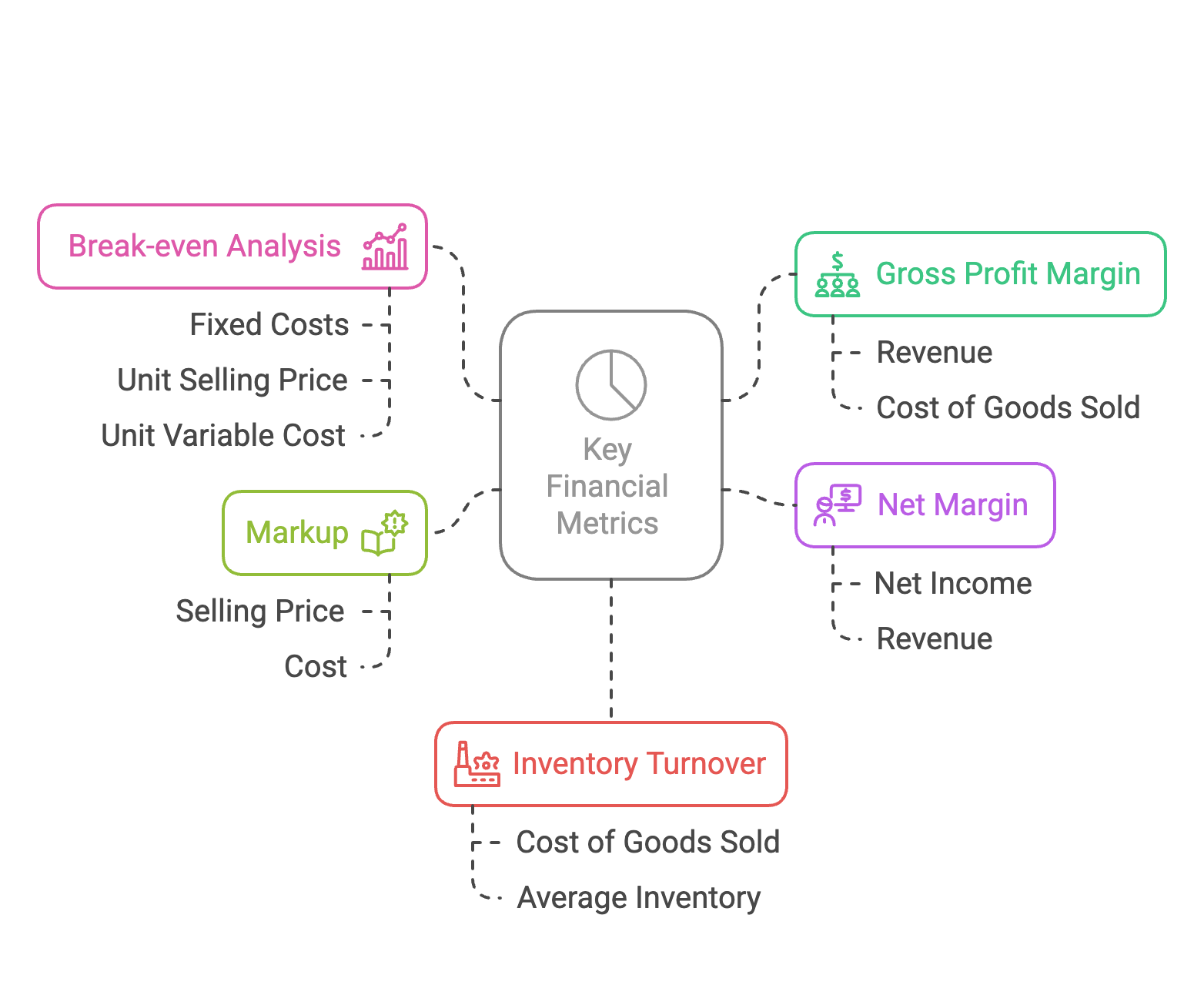

Key Financial Metrics

Tracking specific metrics gives you a clear picture of your wholesale operation’s financial health:

- Gross Profit Margin (GPM): (Revenue – Cost of Goods Sold) / Revenue

Helps assess core profitability before overhead. - Net Margin: Net Income / Revenue

Reveals true profitability after all expenses. - Markup: (Selling Price – Cost) / Cost

Ensures you price products with enough margin to cover overhead. - Break-even Analysis: Fixed Costs ÷ (Unit Selling Price – Unit Variable Cost)

Pinpoints when you begin making a profit on each product line. - Inventory Turnover: Cost of Goods Sold ÷ Average Inventory

High turnover indicates effective stock management. A median wholesale trade company sees about 6.4 turns per year.

These metrics inform pricing, highlight inefficiencies, and reveal whether you need to adjust your purchasing or payment strategies. They also create a dashboard for spotting potential problems, such as stagnating inventory or razor-thin margins.

Payment Cycles and Receivables

In wholesale, offering credit terms is normal, but extended timelines (Net 30, Net 60, or longer) can disrupt your cash flow. Data shows that the average payment term in the wholesale sector grew from 33 days in 2019 to 61 days in 2022, with 45% of wholesalers extending terms beyond pre-pandemic levels. These delays tie up your cash in unpaid invoices.

Strategies for Healthy Receivables:

- Early Payment Discounts: A small discount, such as 2% for payment within 10 days, incentivizes swift payments.

- Credit Assessments: Check prospective clients’ creditworthiness before granting substantial credit lines.

- Automated Reminders: Use invoicing tools or Overjoy AI for timely follow-ups.

- Factoring (If Needed): Sell receivables to a factoring service, gaining immediate liquidity at a discount.

Keeping Days Sales Outstanding (DSO) low boosts your overall cash flow, preventing a cycle where you constantly scramble to pay suppliers while waiting on customers’ checks.

Managing Cash Inflows and Outflows

Wholesalers often pay for inventory far in advance of collecting payments. To stay balanced, monitor both revenue timing and expense patterns. A rolling forecast clarifies whether your upcoming inflows can cover short-term obligations:

- Gather Historical Data: Review last year’s sales, costs, and demand spikes.

- Project Future Periods: Estimate revenue and expenses for each upcoming month or quarter.

- Update Continuously: Replace old estimates with actual results to refine future forecasts.

Rolling forecasts can boost budget accuracy by about 14% compared to static annual budgets. Even a simple spreadsheet approach can reveal seasonal shortfalls and prompt you to secure financing or delay large purchases strategically.

Financing Options and Strategies

When cash gaps emerge—perhaps due to early inventory investments or a surge in late payments—financing can bridge the shortfall:

- Bank Lines of Credit: Provide a flexible safety net for day-to-day cash needs.

- Factoring: Convert unpaid invoices into immediate cash, paying a fee to the factoring company.

- Short-Term Loans: Ideal for one-off needs, like inventory purchases for a major seasonal event.

About 37% of wholesalers with 90+ day payment terms use supply chain financing programs to survive liquidity crunches. Always compare costs (interest, fees) against potential gains in free cash flow or lost sales if you don’t act.

Pricing Strategies and Cost Structures

A well-thought-out pricing framework must factor in your Cost of Goods Sold (COGS), overhead (rent, utilities, payroll), and variable costs (shipping, packaging). Done right, pricing can safeguard your profit margin without driving customers away:

| Cost Component | Description | Influence on Wholesale Pricing |

|---|---|---|

| COGS | Materials, manufacturing, or procurement costs | Forms the baseline for markups |

| Overhead | Fixed business expenses (e.g., rent, salaries) | Determines minimum revenue thresholds |

| Variable | Expenses that scale with sales volume (e.g., freight) | Requires ongoing monitoring to adjust pricing when volumes shift |

The average wholesale distribution company runs with about 3.4% free cash flow, so every percentage point saved in COGS can significantly enhance profitability.

Inventory Management and Demand Forecasting

Wholesale inventory can be large and costly, tying up capital if demand softens or delayed if you stock out. Balancing supply and demand is crucial:

- Economic Order Quantity (EOQ): A formula to optimize order sizes, reducing per-unit handling and holding costs.

- Demand Forecasting: Use historical sales data, market trends, and predictive tools to anticipate future orders.

- Automated Tracking: Systems like Overjoy AI or ERP solutions can send alerts when demand spikes or inventory dips too low.

Some wholesale distributors achieve a cash-to-cash cycle as short as 15.9 days. They accomplish this by keeping inventory lean and swiftly converting stock into paid orders.

Logistics, Distribution, and Cost Reduction

Cutting extraneous costs and improving turnaround times strengthens your cash flow. Consider:

- Warehouse Management System (WMS): Automated picking and packing reduce labor and errors.

- Route Optimization: Streamlined shipping routes lower fuel costs and accelerate deliveries.

- Supplier Collaboration: Negotiating better rates or terms through strong supplier relationships cuts overhead.

Industry reports show that extended payment terms can raise working capital requirements by around 18%. By integrating efficient logistics, you shorten the time between paying your suppliers and receiving funds from customers.

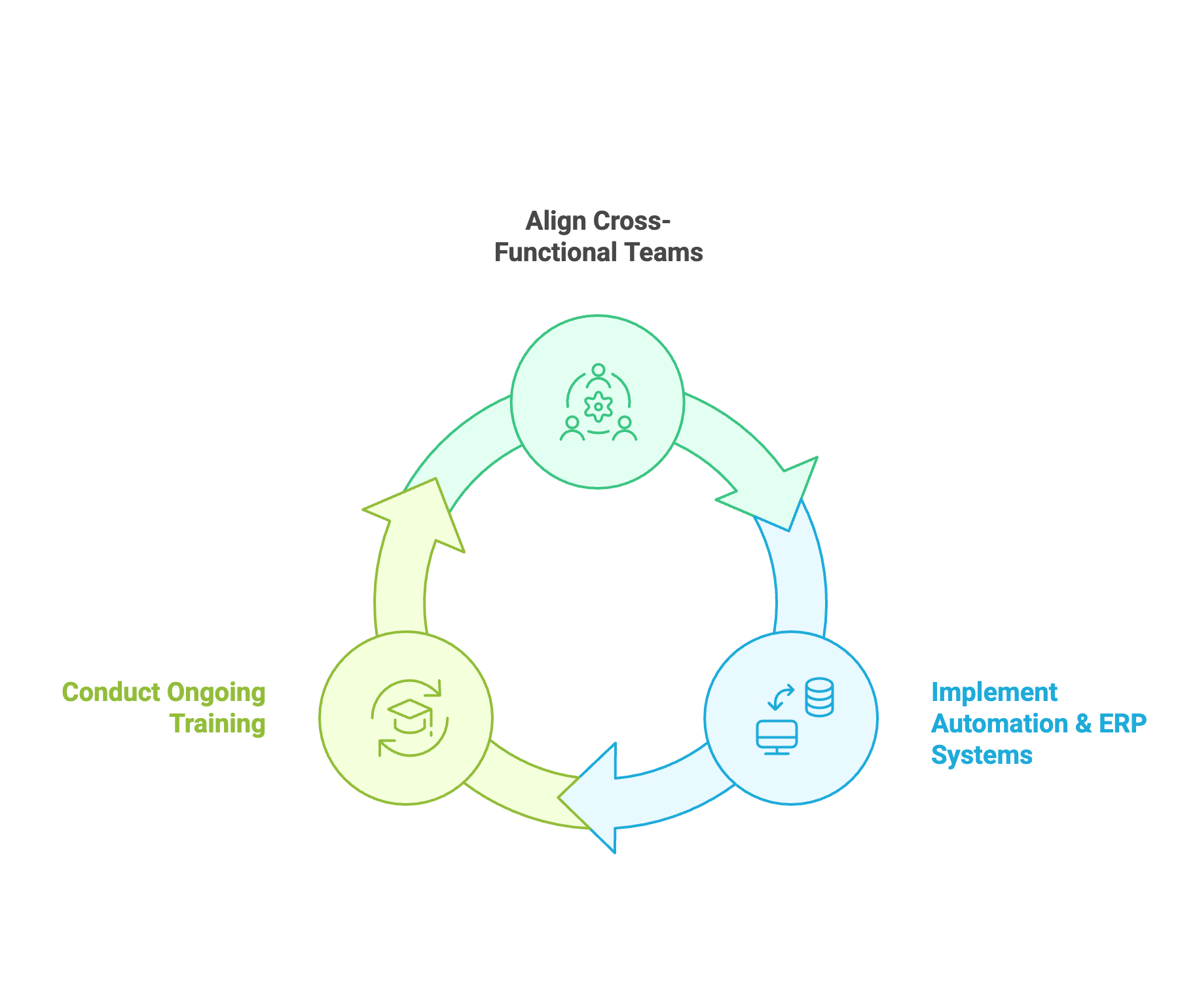

Operational Efficiency and Continuous Improvement

Lean methodologies and regular process reviews help you spot waste or inefficiencies. Focus on:

- Cross-Functional Teams: Encourage sales, finance, and operations to align on forecasts, orders, and payment terms.

- Automation & ERP Systems: Centralize data for real-time insights, reducing duplicate tasks and manual errors.

- Ongoing Training: Support staff development so everyone understands how financial decisions affect the business.

In one survey, 62% of wholesale/distribution CFOs reported better operating cash flow, largely thanks to improved processes and clearer cross-department communication.

Risk Management and Mitigation

Wholesale operations face risks like currency fluctuations, supply chain disruption, or customer defaults. Minimizing these threats reduces revenue volatility:

- Emergency Funds: Keep enough liquid reserves to cover at least three to six months of operating expenses—a practice followed by 78% of wholesalers.

- Insurance Coverage: Common policies include business interruption, property, or liability.

- Customer Diversification: Avoid relying on one or two large buyers. Spread your market exposure for stability.

Regularly reviewing your invoices, inventory turnover, and customer payment histories can highlight early signs of trouble—whether it’s a client on the brink of default or an impending drop in demand.

Compliance, Regulations, and Best Practices

Operating compliantly prevents fines or disruptions and promotes trust among suppliers and buyers:

- Record-Keeping: Document all invoices, payments, and supplier agreements thoroughly.

- Tax and Legal Requirements: Understand import/export laws, state or national tax codes, and licensing.

- Industry Standards: Stay current on best practices that can improve day-to-day operations and align financial protocols with broader market norms.

Some wholesalers extend credit beyond 60 days. If you do, ensure your practices align with applicable credit regulations and that all paperwork remains in order.

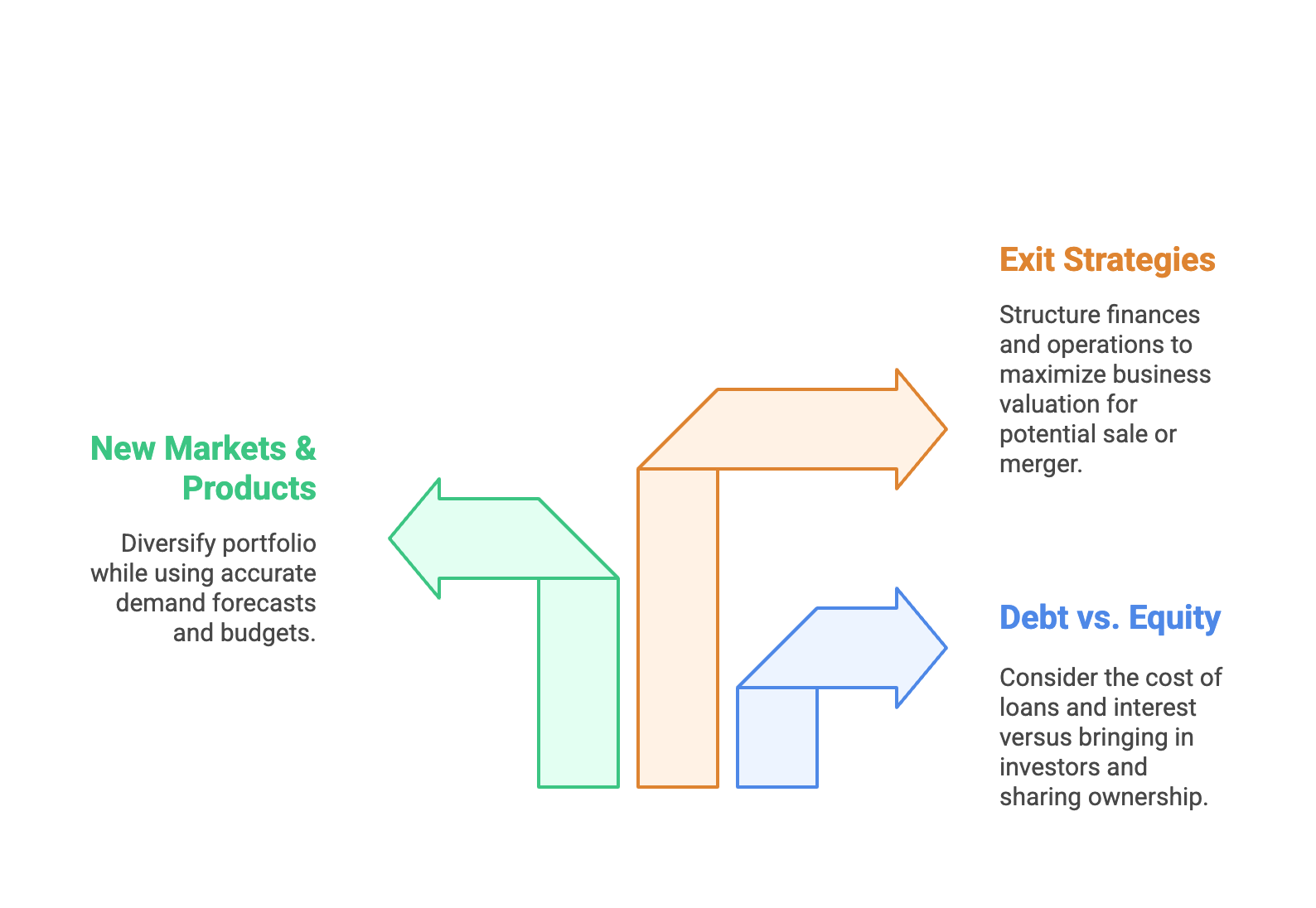

Strategic Growth and Long-Term Planning

Balancing near-term cash flow with future ambitions is key to sustainable growth:

- Debt vs. Equity: Weigh the cost of loans and interest against bringing in investors and sharing ownership.

- New Markets & Products: Diversify your portfolio to spread risk, but use accurate demand forecasts and budgets to avoid overextension.

- Exit Strategies: If you plan to sell or merge the business eventually, structure finances and operational processes to maximize valuation.

Surveys show 72% of wholesaler CFOs extended payment terms to customers, with 53% concerned about the long-term impact on liquidity. As you expand, measure how each financial move—like offering lenient credit—affects both current funds and strategic objectives.

Conclusion

Strong wholesale finance demands vigilance, flexibility, and collaboration across your organization. From setting the right credit policies to managing high-volume inventory, every decision affects your bottom line. Key reminders:

- Prioritize Liquidity: Even profitable wholesalers can stall if cash is tied up in inventory or unpaid invoices.